Built for Small Business

Separate Business and Personal. Finally

Dedicated workspaces for your business finances. Track expenses, manage business debt, and keep everything clean for tax time.

Learn moreStop guessing when you'll be free. Spendify calculates your exact payoff date, compares strategies, and shows how extra payments change your timeline.

$530

Avg. Interest Saved

4 mo

Faster Payoff

13,000+

Banks Supported

You graduated, but the debt followed. Most tools make it harder, not easier.

Your loan servicer shows a balance and a minimum payment. They don't show you when you'll actually be free, or how to get there faster.

Federal, private, subsidized, unsubsidized, each with different rates and balances. Tracking them all in one place feels impossible.

Snowball or avalanche? Refinance or don't? Everyone has an opinion, but no one shows you the math for your specific loans.

Built for people with real debt who want a real plan, not another budgeting lecture.

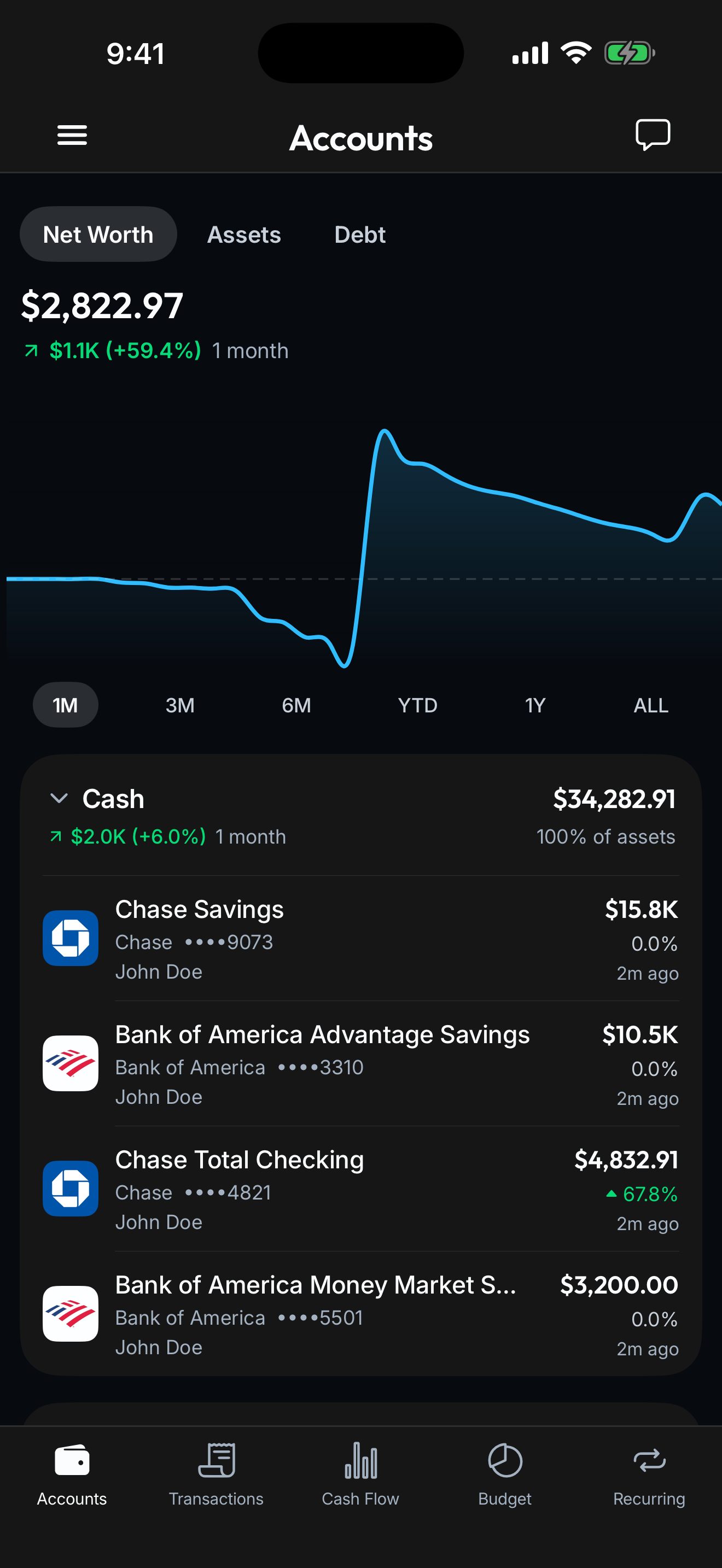

Connect your loan accounts and see the exact month and year you'll be debt-free. Updated automatically as you make payments.

See snowball vs avalanche side by side with your actual loan data. Know exactly how much interest each strategy saves you.

What if you put your tax refund toward loans? What if you add $50/month? Run scenarios and see how your payoff date changes instantly.

Connect your loan servicer through Plaid. Balances, payments, and interest rates stay up to date automatically. No manual entry.

Connect your banks, cards, loans, and investments once. Spendify keeps everything in sync so the whole financial picture stays current without a single spreadsheet.

See how it worksLink your student loan accounts through Plaid. Federal and private loans both supported.

See snowball, avalanche, and custom payoff plans side by side with your real numbers.

Track every payment, watch your balance drop, and see your debt-free date get closer.

Yes. Spendify connects to major loan servicers including Nelnet, MOHELA, Aidvantage, and others through Plaid. Both federal and private student loans are supported.

Absolutely. Connect all your loan accounts and Spendify combines them into a single payoff plan. You'll see a unified debt-free date and can compare strategies across all your loans.

Spendify calculates your payoff timeline and total interest for snowball (smallest balance first), avalanche (highest rate first), and custom priority orders. You see them side by side with your real loan data.

Use what-if scenarios to see how extra payments change your payoff date and interest savings. Try different amounts, even one-time windfalls like tax refunds, and see the impact instantly.

Yes. Every new account starts with the 7-day free trial, with full access to every feature. Cancel anytime.

Yes. Spendify tracks all your accounts: checking, savings, credit cards, investments, and loans. You get a complete financial picture, not just a loan tracker.

Life rarely fits one label. See how Spendify adapts to other chapters.

Dedicated workspaces for your business finances. Track expenses, manage business debt, and keep everything clean for tax time.

Learn more

Shared workspaces, joint debt payoff plans, and full transparency, without merging bank accounts.

Learn more

Compare payoff strategies, track every balance in real time, and watch your debt-free date get closer with every payment.

Learn moreMore on the ideas behind this playbook.

Parent PLUS borrowers may need to consolidate before July 1, 2026 to keep income-driven repayment and PSLF access. Here's who's affected and the exact steps.

Read articleU.S. household debt hit a record $18.8T. Most is 'good', but some is quietly dangerous. Here's how to classify your own debts and what order to attack them.

Read articleConnect your loans and get a plan in under 2 minutes. Try free for 7 days. Cancel anytime.