How should you split your paycheck?

Enter your monthly take-home pay and the 50/30/20 calculator shows exactly how much goes to needs, wants, and savings, plus what that adds up to over a year.

Your Monthly Income

Enter your take-home (after-tax) monthly income.

See your real spending against these targets

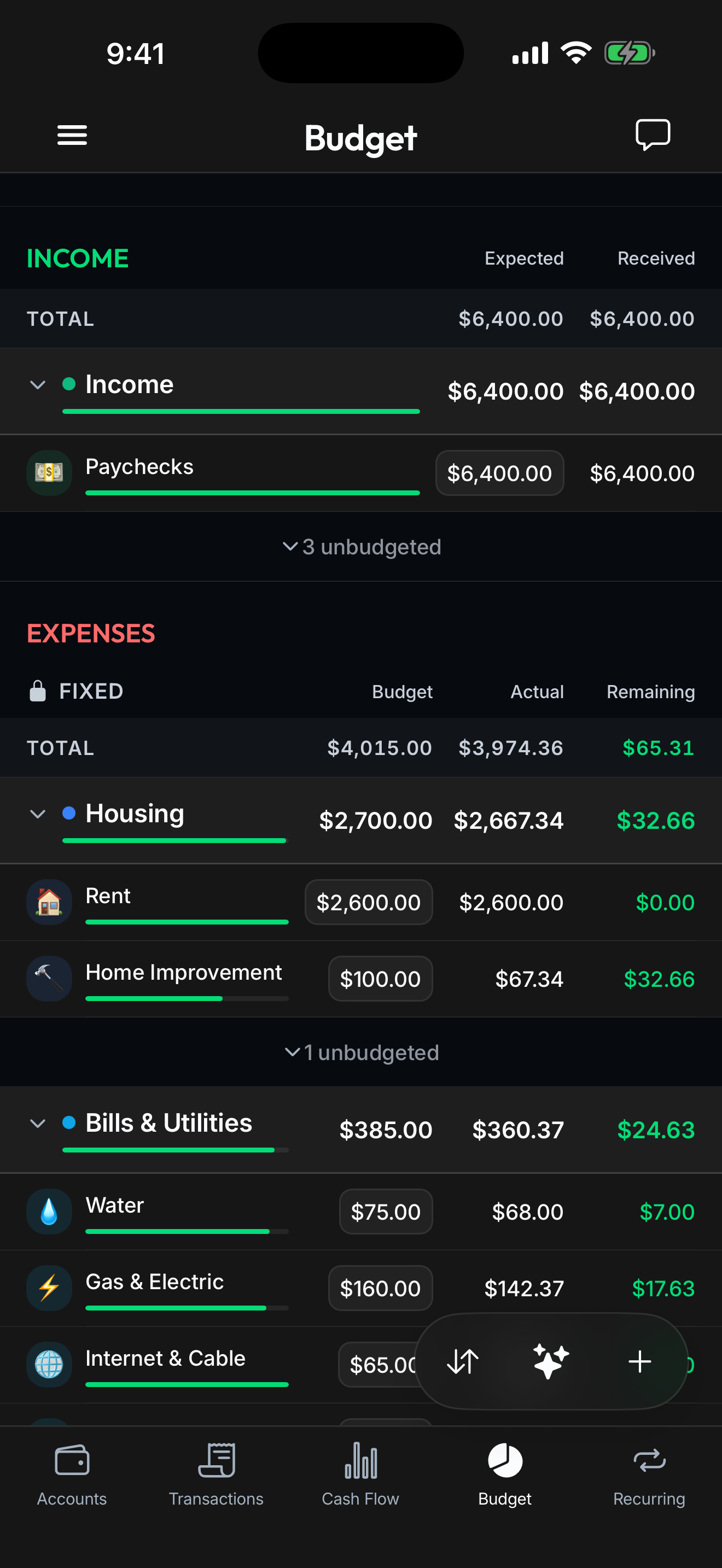

Connect your accounts and Spendify sorts every transaction into needs, wants, and savings automatically, so you always know where you stand against your 50/30/20 plan.

- Auto categorization

- Live budget progress

- Bank connections

- Custom budget targets

- Spending insights

- Monthly recaps

What is the 50/30/20 rule?

Popularized by Senator Elizabeth Warren in All Your Worth, the 50/30/20 rule is the simplest budgeting framework that balances living well today with building for tomorrow.

Needs

Half your income goes to essentials: housing, food, utilities, insurance, minimum debt payments, and transportation. If needs exceed 50%, look for ways to reduce fixed costs.

Wants

Nearly a third for lifestyle: dining out, entertainment, subscriptions, shopping, and travel. These aren't guilty pleasures, they're part of a sustainable budget.

Savings & Debt

A fifth goes to your future: emergency fund, extra debt payments, retirement, and investments. This is where wealth is built and debt is crushed.

What does the split look like at your income?

Here's the 50/30/20 split at a few common monthly take-home incomes. Find the row closest to yours, or use the calculator above for your exact numbers.

| Monthly income | Needs (50%) | Wants (30%) | Savings & debt (20%) |

|---|---|---|---|

| $3,000 | $1,500 | $900 | $600 |

| $5,000 | $2,500 | $1,500 | $1,000 |

| $8,000 | $4,000 | $2,400 | $1,600 |

Numbers not adding up to a budget you can live with? 50/30/20 is a target, not a rule. If housing and groceries push your needs past 50%, start with a temporary 60/30/10 split, then tighten as your income grows or fixed costs drop. If you're focused on debt, fold extra payments into the 20% bucket and pair this with thedebt payoff calculator to see your debt-free date.

50/30/20 budget questions, answered

The 50/30/20 rule is a simple budgeting framework that splits your after-tax income into three buckets: 50% for needs (housing, utilities, groceries, insurance, minimum debt payments), 30% for wants (dining out, entertainment, subscriptions, travel), and 20% for savings and extra debt payments. Popularized by Senator Elizabeth Warren, it's the easiest budget to start with because there are only three categories to track.

Take your monthly take-home (after-tax) income and multiply it by 0.50, 0.30, and 0.20. On a $5,000 monthly income that's $2,500 for needs, $1,500 for wants, and $1,000 for savings and debt. The calculator above does this instantly: enter your income and it shows each bucket plus an annual projection.

If you live in a high-cost area or earn less, needs often take up more than 50% of your income, and that's okay. Treat 50/30/20 as a target, not a hard rule. Trim the wants bucket first, and aim to keep at least some savings (even 5 to 10%) until your income or fixed costs change. The point is a plan you can actually follow.

That's very common with today's rent and grocery prices. First, separate true needs from habits that crept into the needs bucket (a premium phone plan is partly a want). Then attack your biggest fixed costs: housing and transportation. If needs stay stuck above 50%, use a temporary 60/30/10 or 70/20/10 split and revisit as your situation improves.

50/30/20 is faster and more forgiving: three buckets, little maintenance, great for beginners. Zero-based budgeting (every dollar assigned a job) is more precise and better if you want maximum control or are aggressively paying off debt. Many people start with 50/30/20 and graduate to zero-based once budgeting becomes a habit.

Yes, it's 100% free, with no signup or email required. Enter your income and get your full breakdown instantly, as many times as you like. If you want Spendify to track your real spending against these targets automatically, that's the paid app, but the calculator itself is always free.

Want to go deeper on budgeting?

Dive into budgeting strategies and tips on our blog.

Budget Smarter,

Not Harder

Spendify tracks your spending against your budget targets automatically. See where every dollar goes.