Built for Families

Your Whole Household, One Financial Picture

Track household spending, manage family debt, and teach kids about money, with roles that keep everyone in their lane.

Learn moreCompare payoff strategies, track every balance in real time, and watch your debt-free date get closer with every payment.

3

Payoff Strategies

Real-Time

Balance Tracking

13,000+

Banks Supported

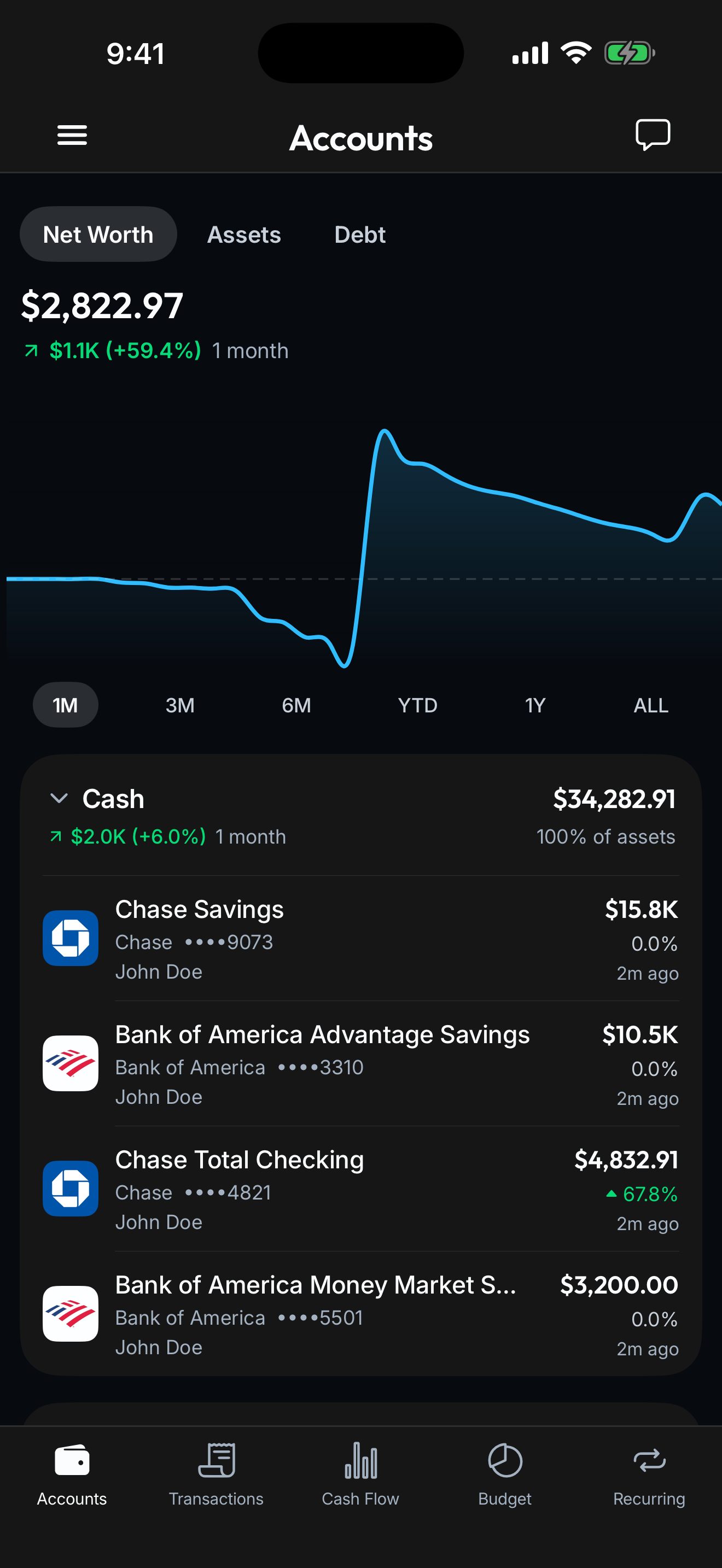

When you're juggling multiple balances, it's impossible to know if you're making progress.

Minimum payments keep you treading water for decades. Without a payoff date, debt feels permanent, because on minimums, it practically is.

Credit cards, personal loans, medical bills, student loans, each with different rates, minimums, and due dates. Keeping track manually is exhausting.

Snowball, avalanche, consolidation loan. Everyone has an opinion. Without seeing the math side by side, you're guessing which approach saves you the most.

Real math, real balances, and a real date when it's all over.

See snowball, avalanche, and custom payoff plans side by side. Compare debt-free dates, total interest paid, and monthly payment schedules for each approach.

Pick a strategy and see exactly when you'll be debt-free. Watch the date move closer as you make extra payments or adjust your plan.

Every credit card, loan, and line of credit synced automatically. Balances update daily so your payoff timeline is always current. No manual entry.

See exactly how much interest you'll save with each strategy. Add $50 extra per month and instantly see the impact on your total cost and timeline.

Connect your banks, cards, loans, and investments once. Spendify keeps everything in sync so the whole financial picture stays current without a single spreadsheet.

See how it worksLink credit cards, loans, and lines of credit through Plaid. Balances, rates, and minimums sync automatically.

See snowball, avalanche, and custom plans side by side. Pick the one that fits your budget and motivation style.

Watch balances drop in real time. Your debt-free date updates automatically as you make payments.

Snowball pays off the smallest balance first for quick wins and motivation. Avalanche targets the highest interest rate first to minimize total interest paid. Custom lets you choose your own payoff order, useful if you want to eliminate a specific debt first, like a family loan.

Yes. Add any extra monthly amount and the planner instantly recalculates your debt-free date, total interest, and monthly schedule. Even $25 extra can shave months off your timeline.

Yes: credit cards, personal loans, student loans, auto loans, medical debt, and mortgages. Any account you can connect through Plaid gets tracked automatically with real-time balance updates.

It depends on your rates and discipline. Spendify helps you compare: run your current debts through the avalanche strategy and see if the total interest is lower than a consolidation loan offer. The math tells the story.

Balances sync daily through Plaid. When you make a payment, the updated balance typically appears within 1-2 business days, and your payoff timeline adjusts automatically.

Spendify uses bank-level encryption (AES-256) and connects through Plaid, the same provider used by Venmo, Robinhood, and thousands of other apps. We never store your bank credentials.

Life rarely fits one label. See how Spendify adapts to other chapters.

Track household spending, manage family debt, and teach kids about money, with roles that keep everyone in their lane.

Learn more

Track irregular income, separate business expenses for tax time, and plan for quarterly payments, without a spreadsheet or an accountant.

Learn more

Track your mortgage payoff date, watch home equity grow in your net worth, and budget for every property expense, all in one place.

Learn moreMore on the ideas behind this playbook.

Parent PLUS borrowers may need to consolidate before July 1, 2026 to keep income-driven repayment and PSLF access. Here's who's affected and the exact steps.

Read articleU.S. household debt hit a record $18.8T. Most is 'good', but some is quietly dangerous. Here's how to classify your own debts and what order to attack them.

Read articleTry free for 7 days. Cancel anytime.