Product Updates Latest

Why We Built Spendify Different

Most finance apps show you where your money went but don't tell you where it should go. Here's the story of why we built Spendify to fill that gap.

Read article

Money tips, debt payoff strategies, and financial advice. Real talk about building financial freedom — no guilt trips.

Most finance apps show you where your money went but don't tell you where it should go. Here's the story of why we built Spendify to fill that gap.

Just landed your first job? Here's a no-nonsense guide to handling your money right from day one, from 401k matches to avoiding lifestyle inflation.

Waiting for the perfect moment to invest? It may never come. Here's how to figure out if you're ready and how to start small.

Not all side hustles are worth your time. Learn how to calculate your real hourly rate and pick opportunities that actually move the needle.

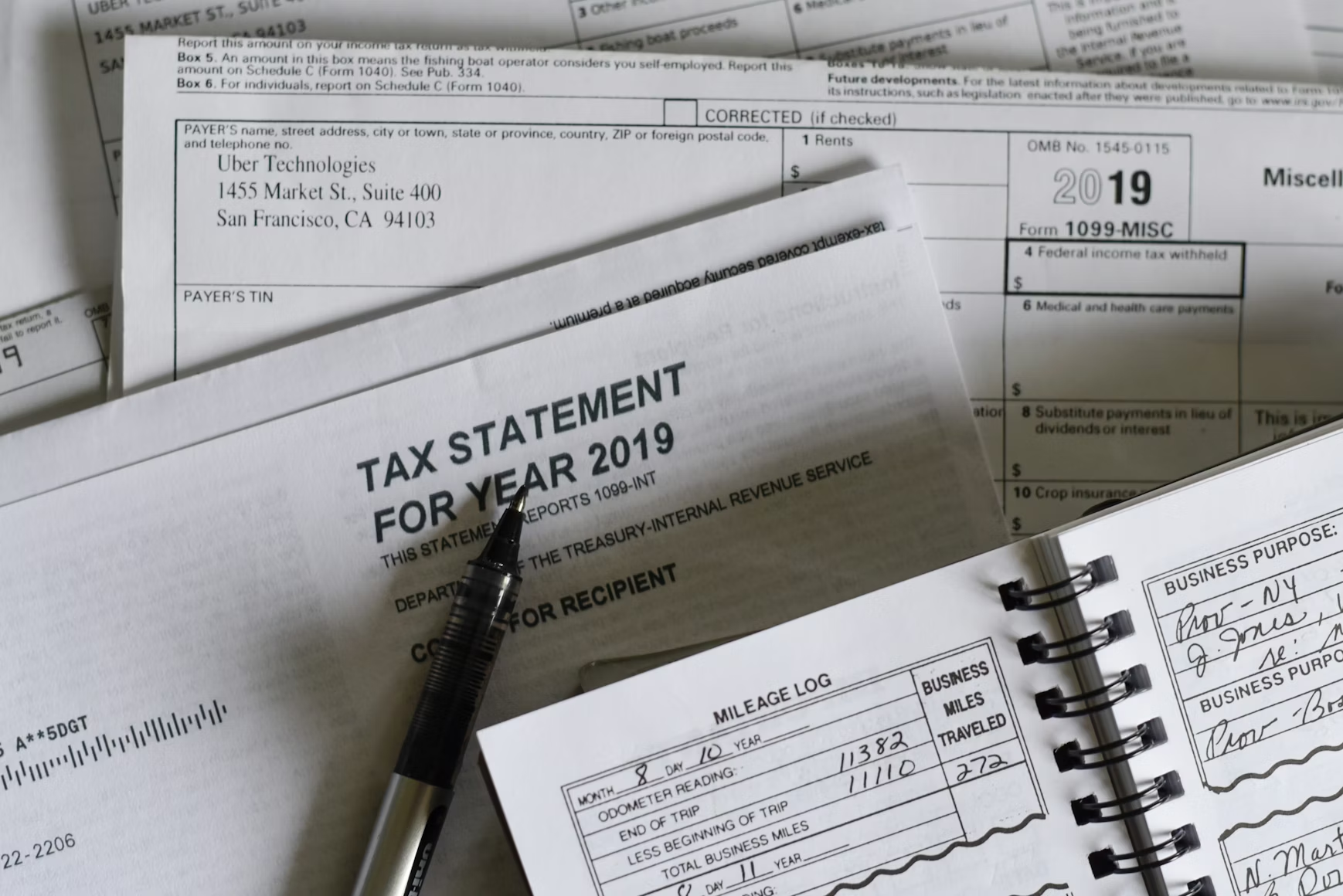

The average tax refund disappears in weeks. Here's a smarter way to split your refund between debt, savings, and fun.

The initial motivation fades around month four of any financial plan. Here's why it happens and practical strategies to push through.

Money is the number one source of conflict in relationships. Here's how to have productive financial conversations with your partner.

No spend challenges are popular, but they can backfire if you're not careful. Here's how to make one work without the post-challenge binge.

Lifestyle creep silently erodes your financial progress every time you get a raise. Learn how to spot it and keep your spending intentional.

Balance transfer cards can save you thousands in interest, but only if you avoid the common pitfalls. Here's what you need to know before applying.

A step-by-step guide to building a real debt payoff plan, from gathering your balances to picking a strategy and tracking your progress.

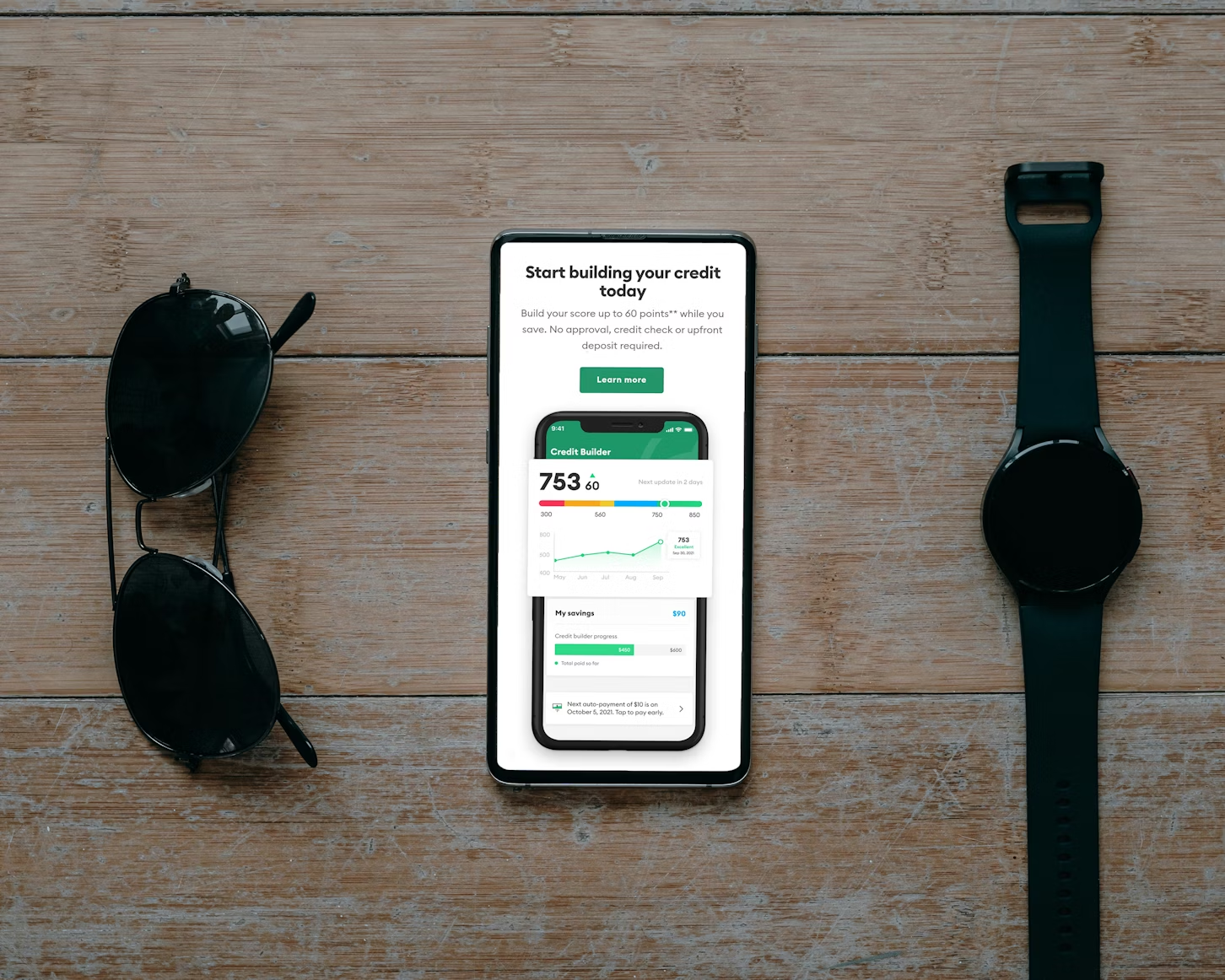

Should you focus on boosting your credit score or paying off debt first? Here's how to decide based on your financial timeline and goals.

Financial stress triggers your brain's threat response, raising cortisol and impairing decision-making. Here's how to break the cycle between money worries and mental health.

Daily expense tracking leads to burnout. A 15-minute weekly check-in is more sustainable and effective for staying on top of your finances.

One bad week doesn't undo months of progress. Here's how to assess the damage, recover, and learn from budget overspending without giving up.

Vague goals like 'save more money' don't work. Learn how to set specific, measurable financial goals and build systems that make progress automatic.

Sinking funds let you save monthly for irregular expenses like car insurance, gifts, and travel so they never catch you off guard. Here's how to set them up.

The subscription economy thrives on inertia. Most people underestimate how much they spend on recurring charges. Here's how to audit your subscriptions and take back control.

The debt snowball and avalanche are both proven strategies, but the best one is the one you'll actually stick with. Here's how to choose based on how your brain works.

The 50/30/20 rule divides your income into needs, wants, and savings. But in high cost-of-living areas, the percentages need adjusting. Here's how to make the framework work for you.

The standard advice says 3-6 months of expenses, but your ideal emergency fund depends on job stability, income sources, and personal circumstances. Here's how to figure out your number.

Shopping triggers dopamine in your brain, and retailers exploit cognitive biases like anchoring to make you spend more. Understanding these tricks is the first step to fighting back.

Most people don't realize where their money goes. Track your spending for 30 days and you'll find dozens of small, forgotten expenses draining your budget.

A $5,000 credit card balance at 22% APR can take 9 years to pay off with minimum payments, costing $6,000 in interest. Here's how to break the cycle.

Traditional budgets fail because they treat you like a machine. Learn how conscious spending and the 50/30/20 framework can help you build a budget that actually works.

Join thousands of people who stopped guessing and started planning. Your future self will thank you.